Dear Investor,

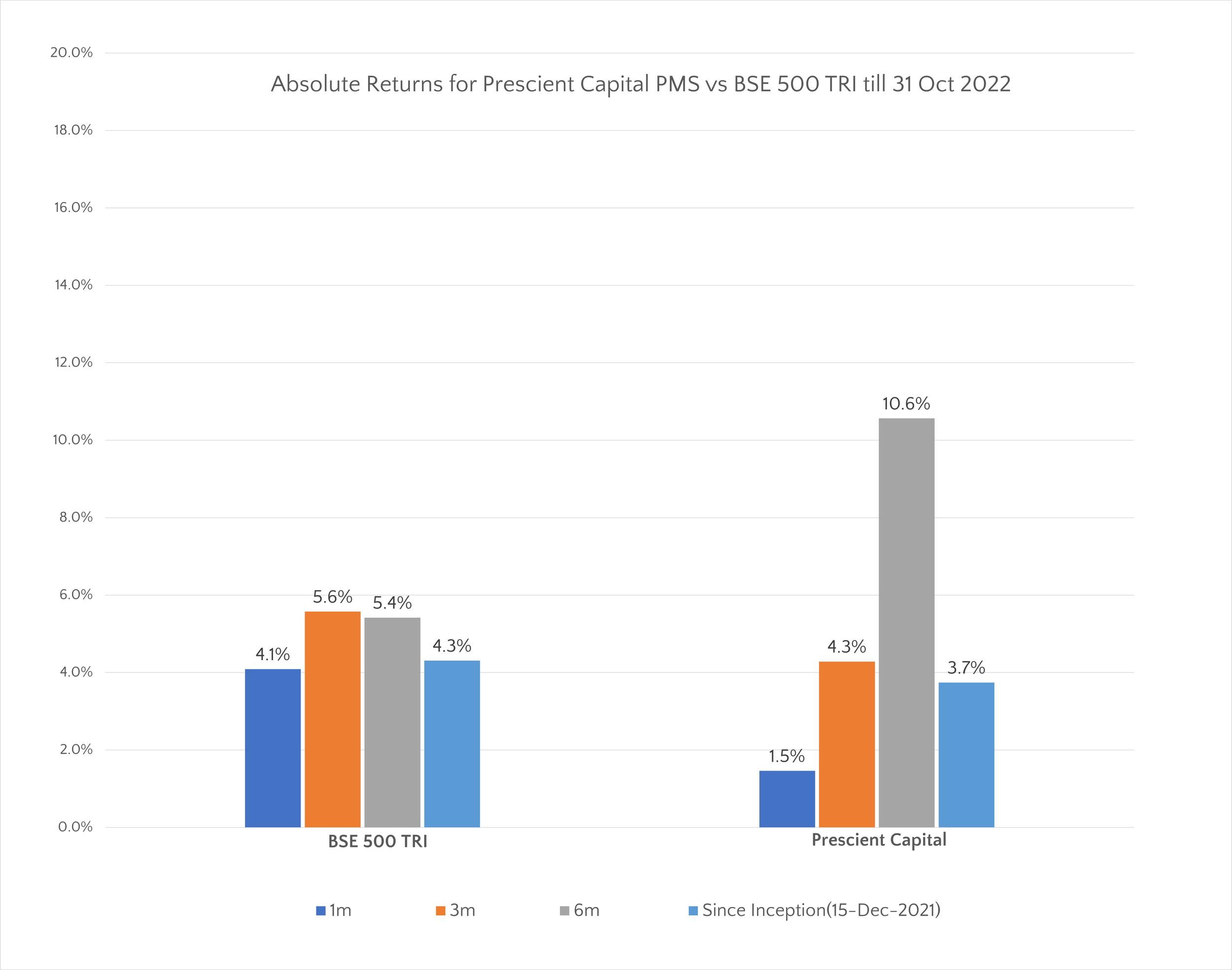

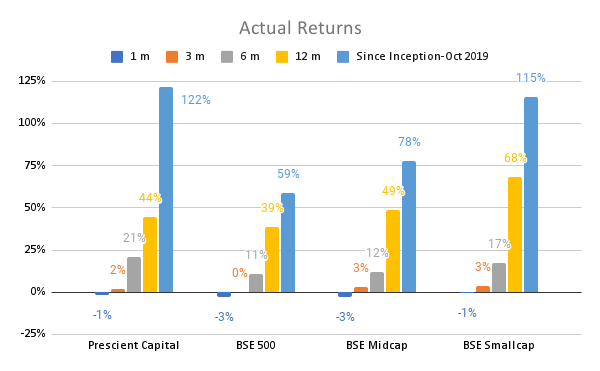

Below chart depicts our performance viz the baseline index.

A lot of you would have read or heard about the recent Hindenburg report on the Adani Group. In this memo, we wanted to draw a parallel from that report and write about why in investing a promoter’s corporate governance is more important than his/her business and/or its valuation. We at Prescient Capital follow the following framework, in that order:

Good/clean promoter

Good business

Good price

Through our decade long journey in investing, we have seen that:

The single largest source of value destruction in markets is a promoter with a chequered governance track record.

Promoter quality is not a linear scale that can be priced in valuation. A lot of our peers think otherwise.

We typically end up investing in small and mid-cap companies which have low institutional shareholding as large institutions/MFs cannot build a sizable position without affecting the price. Third party diligence therefore doesn’t exist or is minimal. Whatever needs to be done is your own independent research. Our promoter research is a mix of both subjective/objective assessment.

In this memo we will try to lay out our promoter governance/evaluation framework which we think is quite robust. The framework has help us significantly reduce the odds of permanent loss of capital.

Promoter/Promoter Group members salary

The ministry of corporate affairs, lays down the maximum limit of remuneration that a Managing Director, Wholetime Directors of a company can together draw as 11% of PAT. Any increase in the absolute value of remuneration of Managing Director, Wholetime Directors should be approved in the AGM. We, however, adopt a more pragmatic commercial stand to the same, as many promoter families fill their middle management ranks with their family members.

We believe that the sum total of salaries of all these family members should not exceed 5-7% of the PAT for that year.

We have often seen red flags whereby a young son of a promoter with a mediocre education background is drawing a salary higher than a senior professional with greater than a decade of professional service experience.

We also raise a reg flag if the salary of a promoter is low. We have come to learn that “less is bad”. A promoter who discloses and takes a flat high remuneration, is far better than the one who draws less and then finds ways to create leakages in the company. Leakages are in the form of movable assets, related party businesses, inducting more than reqd. family members, entering new businesses that match the promoter's lifestyle.

Same applies to the salaries of the key management. Less is bad. Will share an instance about an apparel company, in which the fund we previously worked at, invested in. The salary on the books for two senior business heads was very low. We were invited to a new EBO launch and to our surprise saw them both getting out of their own expensive luxury cars. When we casually enquired about the same with the promoter, the promoter in a sheepish manner, mentioned “They work hard, have given them cars to rest well during their commute!!”. We knew we had a lemon. We soon found out that the balance sheet of that company was completely fake.

We also investigate instances where the salary of a promoter/group is growing higher than the rate of growth of profit of the company. For instance, in 2017, Neeraj Kanwar, the MD of Apollo Tyres asked shareholders for a 43% raise in salary whereas the profits of the company declined by ~ 2%. The shareholders of the company rejected the salary raise and the promoters were forced to take a salary cut. The profits of the Apollo group in FY 2022, are still lower than those in FY 17 and FY 16.

Some promoter groups use buyback to get disproportionate pay out of their companies. The procedure for applying for a buyback is cumbersome for an individual investor and hence their allocation is sometimes unused. Some promoter groups participate in the buyback and get a preferential allocation of the shares not tendered. Groups that use the buyback to their advantage, are a clear pass.

Auditors Remuneration & Diligence

Auditors remuneration is a key monitorable both in absolute terms and as a trend. We are not a big fan of Big 4 or Big 10 in the Indian context, but we question things like: How can an auditor audit a 1000 cr + topline company for 7 Lakh of fee? Sometimes, it just doesn’t add up. This is a huge problem we grapple with Pharma, Speciality Chemicals, Building Material and Consumer Durables Companies in India. The Auditor's salary just doesn’t add up. How can one audit a multi-location plant, sales, distribution set up having a 1500 cr plus topline in less than 25 Lakh? Not saying that these companies are bad, but one needs to find ways to get comfort that they are professionally managed.

Speaking with auditors or someone in the team is a good thing to have. We remember speaking with the auditor of a leading bag company. We had called them to know about the promoters. To our surprise, the auditor told us that the company is involved in a VAT fraud.

We also use our auditor/CA network to identify/meet companies respected in the CA community.

Scanning for related parties:

We typically find related party dealings more than 20% of the sales or purchase of materials as a red flag. On one hand, it diminishes the assumptions of MOAT of a business, on the other, as public market investors we do not have the wherewithal to question the fairness of the dealings event when audited by the Big 4.

We have seen instances, where related party dealings in raw material purchase brings about volatility in margins. We prefer to stay away from such companies. In some cases, promoters take a loose approach and do not mention a competing business by a family member, as a related party. Such companies and groups are a big no.

We also dig for other listed/unlisted promoter entities at the same registered address by looking at websites such as ZAUBA. In case, there is a web of these entities or they have dealings in politically sensitive sectors such as mining, infra, real estate, we stay away from that group.

Some Promoter groups use their family members for key roles like procurement, HR, business development. We prefer to scrutinise these companies more as we understand it is quite easy to fake bills under a family member and syphon funds.

Some promoter groups have inter-corporate deposits (ICDs) where they use cash-flows from one business to support the expansion of the other. The logic often given to minority shareholders is that ICDs will yield more coupon that a treasury yield and hence a win-win for both. In our experience, such groups rarely create value for minority shareholders.

Hidden Liabilities & Receivables

It has been often seen that long term assets and liabilities are a way to brush current receivables and liabilities under the rug. Sectors such as EPC, construction, IT provide an opportunity for milestone-based revenue booking. Promoter groups often use the same to show lower receivables days and impress the investor community.

Inventory write down/off practices in businesses such as apparel, building materials are a way to understand how professional/conservative a promoter is? We have often seen inventory not being written down aggressively to protect the projected profitability and value of assets of a business with shareholders and lenders respectively. Such businesses require one headwind, and the business suddenly turns to red from black.

Business with government/industry bodies with poor credit history

We avoid companies working solely with the government, pseudo government bodies, and development agencies. Dealing with these bodies on social/health/infra projects is a complex task and has been seen to stretch the balance sheet of a company. We cannot quantify this risk and hence stay away from companies such as the Adani Group.

Credit rating by rating agencies

Per us, CRISIL is the only rating agency in India that still does its job diligently. We have seen CRISIL downgrade a promoter group debt due to its inability to pay interest on time or pull back its assessment if the promoter group doesn’t cooperate in CRISILs diligence.

The ultimate test of cash generation of any company is its ability to pay its liabilities (debt & interest) and shareholders (dividend/buyback). We have seen scenarios whereby on one side a company has a significant cash on its books but still delays payment of debt interest and/or principle. Such groups are a red flag.

How distracted or disciplined is a founder

We started this as an informal exercise a decade back but soon realised that this is core. What we are digging for is “How distracted is the founder”. We use this for elimination, rather than for selection. For instance, the MD of a leading consumer durables company being a Lok Sabha MP is a red flag. Or the MD of a leading men apparel brand was more bothered about his silverware, planes, and snow cars than his plans to turnaround his business.

We also look for expansion/acquisition into arguably not related areas. We made the mistake of investing in a gaming company knowing fully that gaming is a non-linear acquisitive business. The promoters of the business recently decided to buyout media companies producing gaming content and a gaming hardware/accessories company. The rationale given was to own the gaming ecosystem. The business has been dumped by most public market investors.

Promoters who become dealers/brokers for their stocks by talking about share blocks need more diligence.

We look for candour in annual disclosures. We look for behaviour whereby a promoter takes undue credit for a macro tailwind in a business and/or delays disclosure of bad news.

Lastly, we are all for a company being run by a professional management. We, however, believe that a management just incentivised by salary/bonus is usually not aligned with the long-term sustainable growth of the company. We stay away from companies where promoters have given the day-to-day control of their business to a management and have not incentivised them by reasonable ESOPs. Such promoters are kept away from the reality of the business by their management.

Look for events of shareholder wealth creation

This is a litmus test that is above all. Prior behaviour of founders to distribute cash reserves, not dilute minority shareholders, high dividend pay-out, not participate in buybacks, and no event of a preferential allotment are all very strong indicators of a good governance.

Another event to measure the same is the terms of merger of a group entity. We do not like promoters who merge/de-merge group entities too often. If done too often, it is usually good only for founders.

Also, a promoter who pledges his stake for equity infusion in another business is a big no. Usually such companies are not left with much chance and your wealth creation (already a low prob) is not aligned with that of the Promoters.

Thanks

Prescient Capital